At WiseGEEK, we're committed to delivering accurate, trustworthy information. Our expert-authored content is rigorously fact-checked and sourced from credible authorities. Discover how we uphold the highest standards in providing you with reliable knowledge.

What are the Basics of Payroll Preparation?

Every employer, large or small, must provide for the periodic payment of wages, commissions, and salaries to its employees. A complex job in the United States, an enterprise's payroll preparation consists of a number of different tasks, including verification of the compensation due to employees, calculation of income and payroll taxes to be withheld from pay, and the calculation of other amounts to be withheld. Although apparently a mundane task that's basic elements remain unchanged from one week to the next, payroll preparation is an absolutely critical element of any business' success, because problems with payroll lead to a dramatic decline in employee morale.

The first element of proper payroll preparation is determining how much each employee is to be paid. Salaried employees are the easiest to pay, because they receive the same amount every week. Hourly employees generally record the time they start and end work on a timekeeping system, and these records are used to calculate their pay. A complicating factor in the calculation of hourly pay is overtime, paid only to hourly employees but at a higher rate than their regular pay. Commissioned employees are usually paid on the basis of their sales, which requires that the relevant sales figures for each salesperson be provided to the payroll department in a timely manner. Commission calculations can be complicated when salespeople work together on a sale and split the commission, as well as by differing commission rates for different products.

Some employers also make additions to their employees' pay, in the form of bonuses, vacation pay, holiday pay, and sick pay, which are taxable, and reimbursement of business expenses, which generally are not taxable. Other adjustments to employees' pay that might be processed through a payroll are the reimbursement of moving expenses and the payment of car and gasoline allowances. There are also different arrangements made to regularize the compensation of commissioned salespeople to help them deal with the extremes of high and low periodic pay that characterize the compensation of commissioned salespeople.

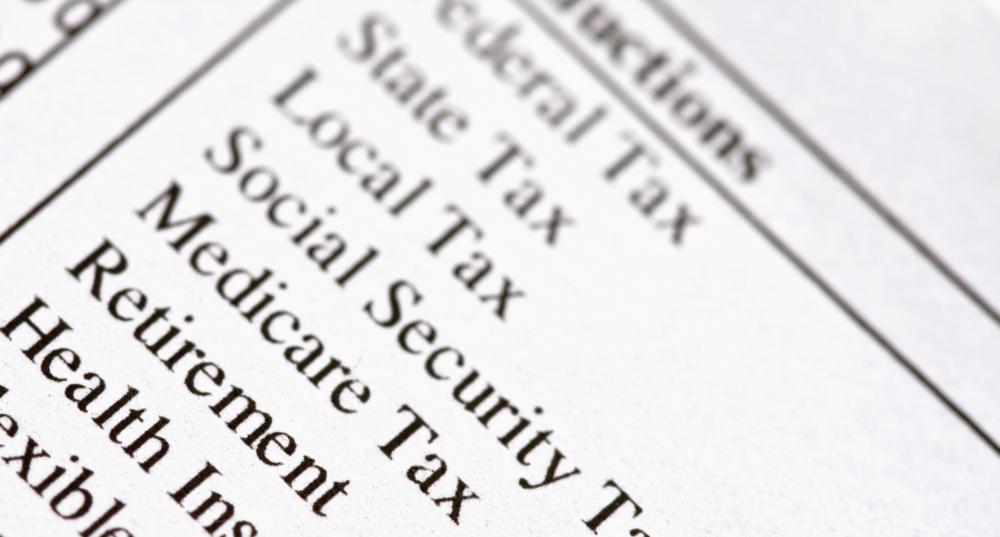

Once the income for each employee has been ascertained, withholding and deductions must be calculated. Payroll taxes for Social Security, Medicare, unemployment, disability and workers compensation must be withheld from every pay subject to statutory requirements and limits, and income taxes must be withheld from the pay of all employees whose pay exceeds a statutory threshold. Voluntary deductions such as health insurance premiums, contributions to retirement savings accounts, flexible spending accounts, and other items must also be calculated. An important element of payroll preparation is to determine which adjustments, whether deductions or additions, take place before the calculation and withholding of income taxes, and which take place afterward. An error in making this determination could lead to troublesome tax consequences for the employee.

Once the payroll has been completely prepared, it must be processed. Payroll processing and production has become a highly automated process in the United States, with many payrolls processed by third-party contractors. Whether done in-house or by a third-party contractor, the process generates individual paper paychecks, as well as direct deposits to employees' bank accounts. In addition, payroll preparation includes the creation of detailed and summary statements for the deposit of amounts necessary to cover the checks and direct deposits, as well as for tax and other payments to the appropriate government agencies or insurance carriers. Those responsible for payroll preparation must provide this information to the employer's finance or accounts payable department, whose job it is to ensure that the funds to pay employees are available and properly deposited. Processing a payroll also includes accumulating the data necessary for the company's periodic financial statements and for producing employees' year-end tax statements. Each payroll is unique, and must be properly and thoroughly prepared before it can be processed, whether in-house or by a third party.

AS FEATURED ON:

AS FEATURED ON:

-

![A payroll administrator handles a company's employee payroll.]() By: alexskopjeA payroll administrator handles a company's employee payroll.

By: alexskopjeA payroll administrator handles a company's employee payroll. -

![Payroll preparation includes calculating each employee's deductions and withholdings.]() By: Stephanie FreyPayroll preparation includes calculating each employee's deductions and withholdings.

By: Stephanie FreyPayroll preparation includes calculating each employee's deductions and withholdings. -

![Special adjustments to employee pay, like reimbursement of moving expenses, is part of payroll preparation.]() By: Africa StudioSpecial adjustments to employee pay, like reimbursement of moving expenses, is part of payroll preparation.

By: Africa StudioSpecial adjustments to employee pay, like reimbursement of moving expenses, is part of payroll preparation.

Discussion Comments

@Vincenzo -- but things have improved greatly over the years. A lot of taxes are paid online and calculated by accounting programs. Thank goodness we are far removed from the old days of having to consult paper tax tables to figure out deductions.

One confusing element about taxes remains, though. Why do we still have to file paper forms with the federal government (and a lot of states) from time to time? All of that information is provided online, so what's the point of duplicating it?

@Vincenzo -- a flat tax might make things simpler, but what are the chances of that actually happening? Slim to none, probably.

Besides, think of all the payroll jobs that would be lost if the tax code was simplified with a flat tax.

Dealing with taxes is the worst part of that process by far. The deadlines are pretty well set in stone and both state and federal officials love slapping penalties on people.

It would be fascinating to see just how much money is spent by large corporations on payroll for people who do nothing but process payroll. Some companies do have whole departments but deal with that and nothing else and it can be quite a chore.

A simple, flat tax on wages would take a lot of complexity out of the process.

Post your comments