At SmartCapitalMind, we're committed to delivering accurate, trustworthy information. Our expert-authored content is rigorously fact-checked and sourced from credible authorities. Discover how we uphold the highest standards in providing you with reliable knowledge.

What is Tax Planning?

Malcolm Tatum

Malcolm Tatum

Malcolm Tatum

Malcolm Tatum

Tax planning is a broad term that is used to describe the processes utilized by individuals and businesses to pay the taxes due to local, state, and federal tax agencies. The process includes such elements as managing tax implications, understanding what type of expenses are tax deductible under current regulations, and in general planning for taxes in a manner that ensures the amount of tax due will be paid in a timely manner.

One of the main focuses of tax planning is to apply current tax laws to the revenue that is received during a given tax period. The revenue may come from any revenue producing mechanism that is currently in operation for the entity concerned. For individuals, this can mean income sources such as interest accrued on bank accounts, salaries, wages and tips, bonuses, investment profits, and other sources of income as currently defined by law. Businesses will consider revenue generated from sales to customers, stock and bond issues, interest bearing bank accounts, and any other income source that is currently considered taxable by the appropriate tax agencies.

In many cases, a primary goal of tax planning is to apply current laws in a manner that allows the individual or business to reduce the amount of taxable income for the period. Thus, planning for taxes involves knowing which types of income currently qualify for as exempt from taxation. The process also involves understanding what types of expenses may be legitimately considered as deductions, and what circumstances have to exist in order for the deduction to be claimed on the tax return.

There are three common approaches to tax planning for the purpose of minimizing the tax burden. The first is to reduce the adjusted gross income for the tax period. This is where understanding current tax laws as they relate to allowances and exemptions come into play.

A second approach to tax planning is to increase the amount of tax deductions. Again, this means knowing current laws and applying them when appropriate to all usual and normal expenses associated with the household or the business. Since these can change from one annual period to the next, it is always a good idea to check current regulations.

One final approach that may be applicable to effective tax planning has to do with the use of tax credits. This can include credits that relate to retirement savings plans, college expenses, adopting children, and several other credits. One common example of a tax credit is the Earned Income Credit, which is intended to relieve the tax burden for persons who earn less than a certain amount within a given calendar year.

Malcolm Tatum

After many years in the teleconferencing industry, Michael decided to embrace his passion for trivia, research, and writing by becoming a full-time freelance writer. Since then, he has contributed articles to a variety of print and online publications, including SmartCapitalMind, and his work has also appeared in poetry collections, devotional anthologies, and several newspapers. Malcolm’s other interests include collecting vinyl records, minor league baseball, and cycling.

Learn more...

Malcolm Tatum

After many years in the teleconferencing industry, Michael decided to embrace his passion for trivia, research, and writing by becoming a full-time freelance writer. Since then, he has contributed articles to a variety of print and online publications, including SmartCapitalMind, and his work has also appeared in poetry collections, devotional anthologies, and several newspapers. Malcolm’s other interests include collecting vinyl records, minor league baseball, and cycling.

Learn more...AS FEATURED ON:

AS FEATURED ON:

-

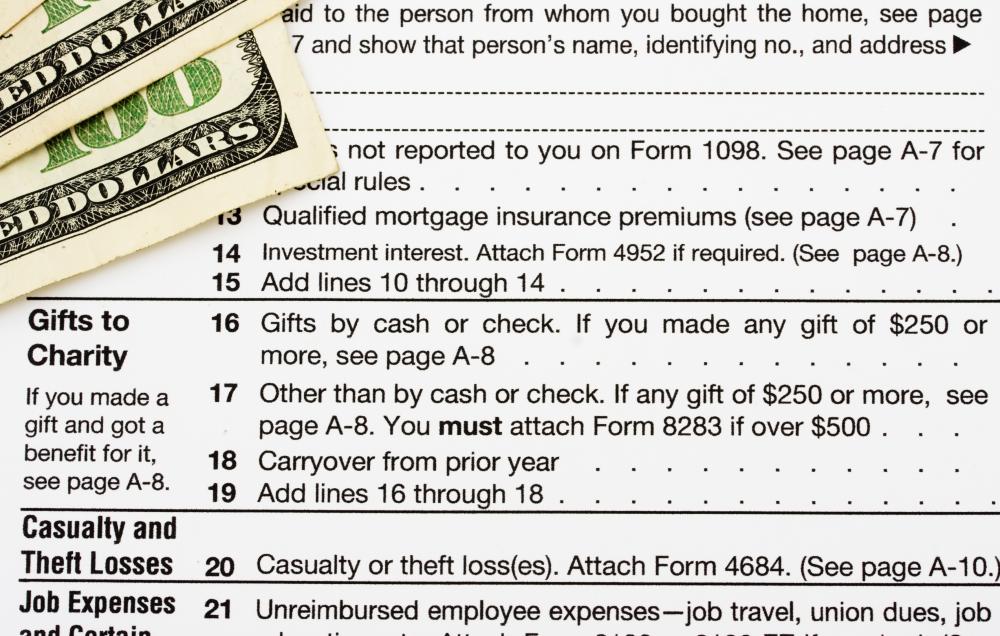

![Part of tax planning is maximizing the amount of deductions one can claim when filing.]() By: Karen RoachPart of tax planning is maximizing the amount of deductions one can claim when filing.

By: Karen RoachPart of tax planning is maximizing the amount of deductions one can claim when filing. -

![Free or discounted tax planning advice may be available for seniors or those with a low income.]() By: nyulFree or discounted tax planning advice may be available for seniors or those with a low income.

By: nyulFree or discounted tax planning advice may be available for seniors or those with a low income.

Discussion Comments

What is the border between corporate tax planning and tax fraud, or is it constantly moving as laws are changing?

If you failed at tax planning in 2010 and ended up owing, the best thing you can do now is to start tax planning strategies for April 2011. My thoughts about a tax refund, even though it's nice, is the government paying you back a year later for money they overcharged you for last year.

Tax planning is essential part of financial planning. it not only helps in saving some money by paying less taxes as tax breaks allow for these savings but also it results into making saving a habit.

Post your comments