At WiseGEEK, we're committed to delivering accurate, trustworthy information. Our expert-authored content is rigorously fact-checked and sourced from credible authorities. Discover how we uphold the highest standards in providing you with reliable knowledge.

What is an Economic Collapse?

Malcolm Tatum

Malcolm Tatum

Malcolm Tatum

Malcolm Tatum

An economic collapse is a situation in which the local, regional, or national economy undergoes a dramatic downturn that negatively impacts the ability of people living in the area to maintain an equitable standard or living. Often, with an economic collapse, major industries fail, jobs are lost, and disposable income is almost non-existent. Typically, even after the economy begins to recover from an economic collapse, that recovery may take years to complete, a fact that leaves lingering hardship for consumers over an extended period of time. While sometimes viewed as a crisis of capitalism, an economic collapse can also take place when the economy is state controlled.

The Great Depression of the early 20th century is often cited as an event that exhibited all the markings of a classic economic collapse. Beginning with the collapse of the stock market in the United States in 1929, this era was earmarked by the closing of many businesses and mass unemployment. As a result, many people lost their homes or were unable to feed their families. Recovery was incremental throughout the 1930s, although many economists believe that the United States was fully recovered by the time the nation entered World War II, a situation that positioned the country to experience an economic boom as industry increased to levels that were beyond those previously projected.

In like manner, the economic collapse of the Russian Federation near the end of the 20th century also led to a lengthy period of recovery. Decreased output combined with low oil prices created the crisis as the nation adjusted to changes that took place after the end of the Cold War. Only as oil prices rallied and further internal adjustments were made did the nation begin to move out of the collapse and into a more prosperous economy.

More recently, the worldwide recession that is generally believed to have started in 2007 has brought about conditions that are associated with an economic collapse. In nations across the world, the crisis undermined the major investment markets, with unemployment increasing significantly. As a result, people began to default on their debts, including mortgages, car loans, and credit cards. By 2010, many nations were entering into a period of recovery, with unemployment in at least a few nations slowing down and the rate of default on bank loans beginning to stabilize and even reverse in some places.

While an economic collapse can be a national or global crisis, it is also possible for a town or region to experience this type of economic reversal. This phenomenon was seen during the middle 20th century in many towns in the American South, where textile plants were a major source of employment in the community. As production of various textile products was outsourced to less expensive facilities outside the United States, local plants at first scaled back operations and ultimately closed. Over time, many of these former mill towns cultivated other forms of industry and were able to stabilize the local economy. Others have yet to fully recover, and continue to experience population drops as citizens move to other areas with more promising economic opportunities.

Malcolm Tatum

After many years in the teleconferencing industry, Michael decided to embrace his passion for trivia, research, and writing by becoming a full-time freelance writer. Since then, he has contributed articles to a variety of print and online publications, including WiseGEEK, and his work has also appeared in poetry collections, devotional anthologies, and several newspapers. Malcolm’s other interests include collecting vinyl records, minor league baseball, and cycling.

Learn more...

Malcolm Tatum

After many years in the teleconferencing industry, Michael decided to embrace his passion for trivia, research, and writing by becoming a full-time freelance writer. Since then, he has contributed articles to a variety of print and online publications, including WiseGEEK, and his work has also appeared in poetry collections, devotional anthologies, and several newspapers. Malcolm’s other interests include collecting vinyl records, minor league baseball, and cycling.

Learn more...AS FEATURED ON:

AS FEATURED ON:

-

![Unemployment number would increase significantly in the case of economic collapse.]() By: PaoleseUnemployment number would increase significantly in the case of economic collapse.

By: PaoleseUnemployment number would increase significantly in the case of economic collapse. -

![Mass unemployment, such as was experienced during the Great Depression, is a classic hallmark of an economic collapse.]() By: pds209Mass unemployment, such as was experienced during the Great Depression, is a classic hallmark of an economic collapse.

By: pds209Mass unemployment, such as was experienced during the Great Depression, is a classic hallmark of an economic collapse. -

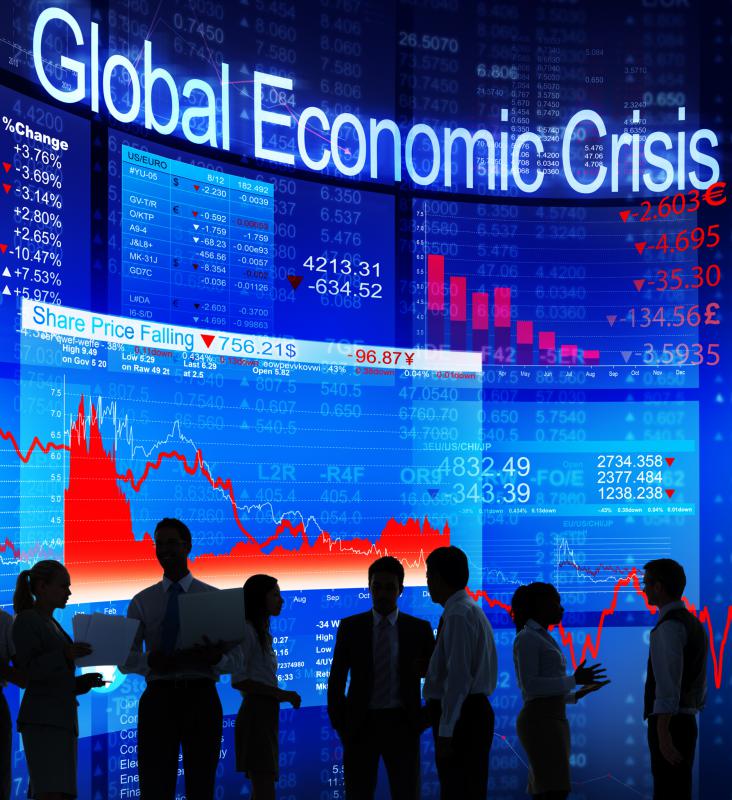

![An economic collapse can be a national or global crisis.]() By: RawpixelAn economic collapse can be a national or global crisis.

By: RawpixelAn economic collapse can be a national or global crisis. -

![At the onset of the recent economic downturn, many people lost significant portions of their retirement savings.]() By: dundanimAt the onset of the recent economic downturn, many people lost significant portions of their retirement savings.

By: dundanimAt the onset of the recent economic downturn, many people lost significant portions of their retirement savings. -

![Issues with homelessness would increase during an economic collapse.]() By: HalfpointIssues with homelessness would increase during an economic collapse.

By: HalfpointIssues with homelessness would increase during an economic collapse.

Discuss this Article

Post your comments